Report: Natural Gas Prices and Utility Infrastructure Spending Have High Impact on Bills; Solar Negligible

In the utility industry’s effort to slow the growth of rooftop solar across the country, electric companies and their trade association, Edison Electric Institute (EEI), have based their campaign on the notion that rooftop solar customers cause a cost-shift to non-rooftop solar customers.

EEI’s Executive Vice President David Owens offers the case. In 2013, Owens said:

“It’s not about lost revenue . . . We want to make sure the grid is maintained, that it can be enhanced, and that cost shifting does not occur.” Also in 2013, in response to an EEI-paid television advertising in Arizona critical of rooftop solar in which a woman tells the viewer, “I shouldn’t have to pay for my neighbor’s solar,” Owens said the ad was about “let’s make sure we don’t shift the costs.”

Owens continued the argument in an interview with the Washington Post in 2015, when he said, “It’s not about profits; it’s about protecting customers … There are unreasonable cost shifts that do occur [with solar]. There is a grid that everyone relies on, and you have to pay for that grid and pay for that infrastructure.” In February 2016, RTO Insider reported that Owens presented the cost shift argument to Wall Street analysts when he made the industry’s case for utility stocks. He further said that utilities are addressing the cost-shift by attempting to increase fixed charges and implement demand charges.

Many reports have rebutted the industry’s cost-shift talking point; one from the Environment America Research & Policy Center analyzed 16 studies and concluded that solar customers do not have a negative effect on non-solar customers. Now, a new report from the Lawrence Berkeley National Laboratory (LBNL), a Department of Energy science lab managed by the University of California, offers the latest evidence that the utilities’ cost shift argument is, for the most part, a self-serving myth.

The report, “Putting the Potential Rate Impacts of Distributed Solar into Context,” set out to find the effect of distributed solar on electricity prices. The results?

The report found that “for the vast majority of states and utilities, the effects of distributed solar on retail electricity prices will likely remain negligible for the foreseeable future.” [emphasis added] Specifically, LBNL finds that distributed solar “likely entails no more than a 0.03 cent/kWh long-run increase in U.S. average retail electricity prices, and far smaller than that for most utilities.”

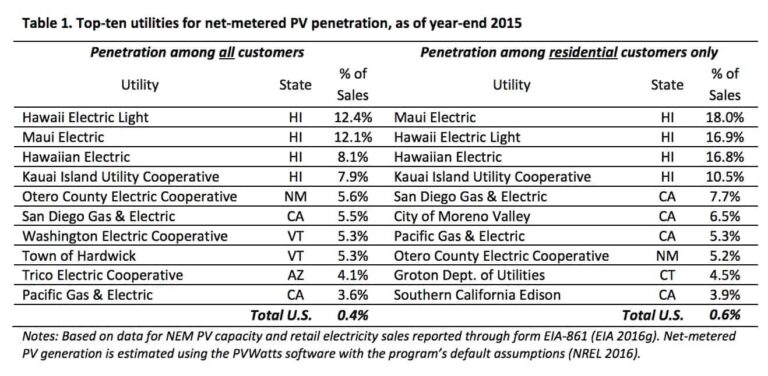

The report further states that for utilities with high solar penetration rates on the order of 10% of electricity sales (all in Hawaii), along with the states set to reach this level by 2030, distributed solar yields between a 5% decrease and a 5% increase in retail electricity prices, assuming distributed solar customers are receiving full net metering volumetric rates (Hawaii regulators have already ended the state’s net metering policy and have replaced it with options that credit customers at lower rates).

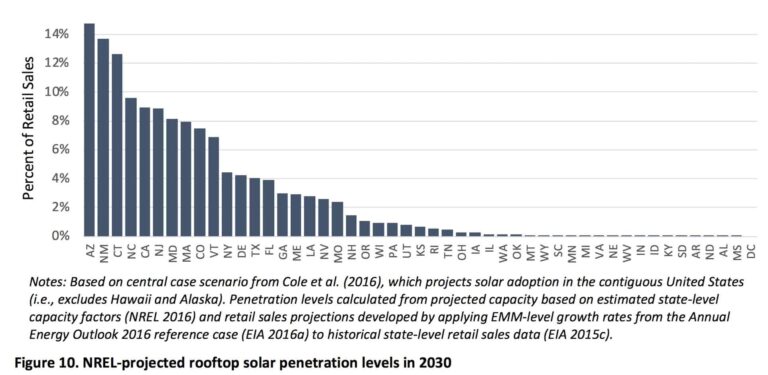

In other words, when distributed solar reaches 10% of electricity sales, the impacts would be either a cost or a benefit of around half a cent/kWh ($0.005/kWh). The figure below is from the LBNL report and it highlights the three states that it estimates will see this 10% penetration level by 2030 (Arizona, New Mexico, and Connecticut).

The report is further proof that utility companies have been less than fully truthful in their concern over cost-shifts. It also provides valuable context to the entire concept of cost shifts, which are rife throughout electricity rate structures, and notes that if utility companies and regulators did want to address price impacts on their customers, they would do better to limit the exposure of customers to the increase of natural gas usage for electricity, and to limit the capital expenditures utility companies propose in rate cases.

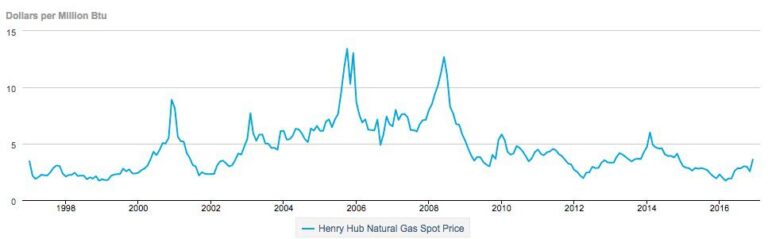

The LBNL report states that “electric sector modeling show that for each $1/MMBtu increase in gas prices, retail electricity prices in 2030 increase by 0.4 cents/kWh (U.S. average) and 1 cent/kWh or more in restructured markets.” The graph below, from the U.S. Energy Information Administration (EIA), shows that natural gas prices are infamously volatile and while 2016 prices average through the entire year were at the lowest level since 1999, an increase of $1/MMBtu is indeed possible by 2030. In fact, the report mentions gas price confidence levels for 2030 range from increases of $2.2 to $5.4/MMBtu.

If regulators and utilities wanted to protect customers from cost impacts, the report recommends limiting the exposure of natural gas by diversifying fuel sources used for electricity generation as one option. Utilities are doing the exact opposite, as many are in the thick of a rush to build natural gas infrastructure. Sierra Club recently released a report that found there is more than 31 GW of gas capacity under construction and 111 GW of proposed gas plants, all of which could result in the construction of more than 200 new natural gas power plants across the country. EIA estimates that the U.S. added 24 GW of new generating capacity last year.

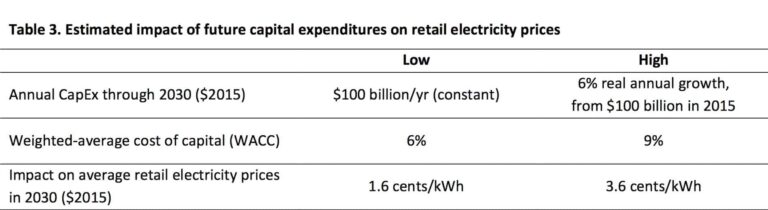

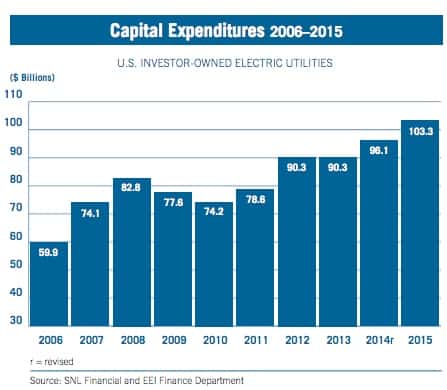

But it is capital expenditures in the electric utility industry that have the largest impact on electricity prices. LBNL says that the cost to customers of anticipated utility capital expenditures is between 1.6 – 3.6 cents/kWh, and unlike solar, there is no scenario where this results in lower power prices for all customers.

For context, according to EEI, “the $103.3 billion spent in 2015 is 157% greater than the $40.2 billion invested during the 12-month period that ended September 30, 2004.”

It makes sense that utilities don’t want to talk about price impacts that result from building more infrastructure: that’s how they make a profit. They’re more than happy, however, to exaggerate (or invent, in many cases) a supposed solar cost shift if it provides them with a rationale for fighting rooftop solar-enabling policies. That’s much better public relations than acknowledging that rooftop solar provides a threat to the classical monopoly utility business model.

In fact, David Owens conceded utilities’ real motives during a private meeting with utility company CEOs almost five years ago. During a discussion on the rise of distributed generation and net metering, Owens delivered a slide, referring to distributed solar growth, that read, “How do you grow earnings in this environment?” The response from the industry has been either working with groups to repeal net metering laws or by requesting higher fixed and demand changes. This is exactly what has happened in the years since.

Most public utility commissions did not buy the utilities’ flawed arguments. According to NC Clean Energy Technology Center’s 50 States of Solar Report 2016 Review, “Forty-six utilities asked for residential fixed-charges increases of 10% last year.” The utilities were granted only partial or no increases in 79% of the cases, according to the report, and fewer utilities proposed demand charges in 2016. “Those that did found an unreceptive audience among regulators. Not a single commission approved such a request.”

However, utilities are continuing their efforts in 2017. In Indiana, for example, a utility-backed bill is making its way through the state senate that would end net metering by 2027 at the latest, or more likely much earlier when net-metered systems hit 1% of utility demand. In the meantime, the bill would not credit rooftop solar customers at the full retail rate.

According to the National Institute of Money in State Politics, Indiana electric utility companies, and their trade association, Indiana Energy Association, have contributed more than $700,000 to candidates for state races and PACs over the past three election cycles; and Indiana Lobby Registration Commission data reveals that these same companies spent $1.045 million on lobbyists over the past two years.

Solar net metering is growing in Indiana, but it currently makes up one-tenth of one percent of demand, providing a prime example, according to the LBNL study, of a place where any kind of cost shift is a pure myth, but where cutting net metering would surely stunt solar’s nascent growth.

A hearing on the bill is set for February 9. The argument utility companies are using to advance the bill? Cost-shift.