Financial analysts expect decarbonization will benefit utility ratepayers and shareholders

Analysts at Morgan Stanley and Moody’s Investors Service expect that more electric utilities will accelerate their transition away from coal, with major financial benefits for both ratepayers and shareholders.

In a research report last month titled “The Second Wave of Clean Energy,” analysts at Morgan Stanley explained how “the surprisingly low cost of renewables” will drive utilities to close most of the remaining U.S. coal plants over the next decade. Replacing coal with cheaper renewable energy could save electricity customers as much as $8 billion each year, according to Morgan Stanley:

We conducted an in-depth, asset-by-asset assessment of the coal fleet in the US and found that >70 GWs of coal capacity will become economically at risk through the course of the next decade (excluding 24 GWs already scheduled to retire), resulting in coal-fired electricity declining from 27% of total US power in 2018 to just 8% by 2030e. The nationwide benefit to customers from replacing coal-fired power with renewables could be as high as $3-8b/year, we estimate, while at the same time we see a total renewables investment opportunity for utilities of $93-184b.

Cheap renewables mean utilities can more easily reduce emissions

In a separate report, Moody’s Investors Service also assessed some of the financial implications of utilities’ efforts to reduce their carbon emissions, and similarly emphasized the opportunities provided by cheap renewable energy:

As the total cost of renewable power falls below the cost of operating coal plants, utilities are increasingly working with their regulators to accelerate their carbon transition without creating financially stranded assets or significantly increasing electric rates.

The Moody’s report discusses how electric utilities “can more easily achieve sharp reductions in carbon emissions when compared to other top emission producing sectors with high environmental risk” such as the automotive and oil refining sectors. The report also looks at how state regulators and policymakers can help ensure the transition away from coal benefits ratepayers, as well as utility shareholders:

The shift could be structured in a way that will benefit most stakeholders. Ratepayers would benefit from the elimination of some fuel-cost pass-through charges, utilities would grow their authorized rate base and environmentalists would see coal-fired generation assets being retired.

Major utilities could boost earnings by replacing coal with renewables

Morgan Stanley analysts expect that some of the most carbon-heavy utilities could boost their earnings growth by replacing coal with renewable energy, and highlighted Southern Company, American Electric Power, Duke Energy, Dominion Energy, PPL Corporation, and Pinnacle West, the parent company of Arizona Public Service. The report explained the opportunities for these “Second Wave Utilities” to increase earnings for their shareholders:

Driven by the surprisingly low cost of renewables, we believe that carbon-heavy utilities that have not historically led the pack in clean energy deployment will accelerate their earnings growth by pursuing a “virtuous cycle”: shutting down expensive coal plants and investing in cheap renewables. As a result, these “Second Wave Utilities”, which all trade at valuation discounts relative to peers, could achieve a valuation re-rating.

“What we’ve found is, now there is a much greater opportunity to achieve kind of a triple-bottom-line benefit in the sense of customers [through lower bills], the environment and shareholders,” said Morgan Stanley analyst Stephen Byrd in an interview with S&P Global. “There is an opportunity now that we think some utilities will seize on. We don’t know for sure, but we see that opportunity, and we see the benefit that other utilities have achieved with their share price performance that have embraced that opportunity.”

Some major investors have urged utilities to accelerate their decarbonization efforts, shift their lobbying efforts to support climate and clean energy policies, and adopt boardroom reforms such as aligning executive compensation with reducing emissions.

Overbuilding gas infrastructure could slow decarbonization

A key factor that will impact the pace of decarbonization in the power sector is the extent to which utilities build new gas-fired power plants and pipelines over the next decade, instead of renewable energy, as coal fades out of the electricity mix.

Morgan Stanley analysts noted some ways in which their analysis could be wrong, including “more rapid than expected growth in natural gas infrastructure.” But they acknowledge ways that their analysis could also end up underestimating the speed of the transition to renewable energy, such as greater resistance to building new gas-fired power plants by state regulators, or if federal regulations are tightened on coal plants and gas pipelines. The Moody’s report also discusses how “environmental opposition to natural gas projects is on the rise.”

A five-part investigation published last month by S&P Global examined electric utilities’ efforts to build unnecessary gas-fired power plants in several states. That spending on gas-fired power plants and pipelines could result in more than $100 billion in stranded costs, according to a Rocky Mountain Institute report.

How this all sorts out will determine the prospects for decarbonizing the U.S. electric grid and will shape the future of the U.S. power sector for decades to come.

S&P Global investigation exploring oversupply in the power sector and the factors driving a glut of natural gas-fired power plants

Decline of coal is certain

Despite that uncertainty, both analysts’ reports made clear that coal would continue to decline. Morgan Stanley analysts expected coal to account for 8% of US electricity generation by 2030, while Moody’s analysts put the figure at 10%. Moody’s also noted explicitly that “Federal and state actions to support the coal industry are not significant enough to halt the decline in thermal coal consumption.”

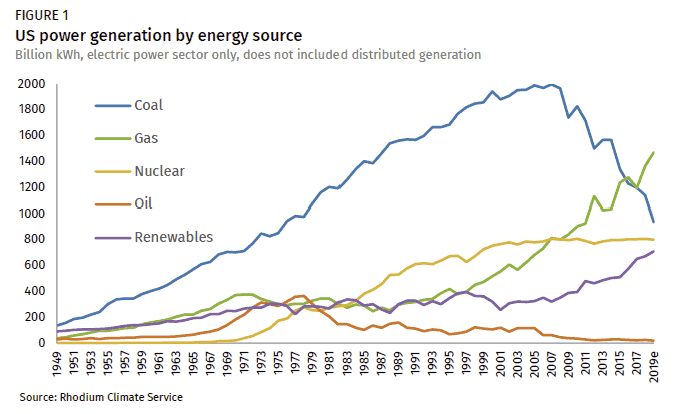

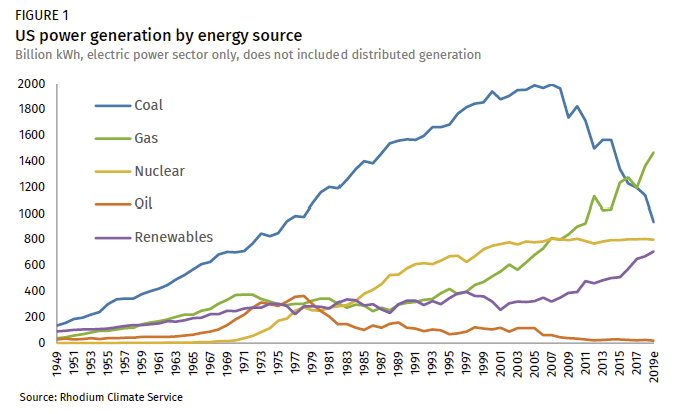

That decline is well underway, and accelerated last year. An analysis by Rhodium Group this week noted that “coal-fired power generation fell by 18% in 2019 (Figure 1). That’s the largest year-on-year decline in recorded history with coal generation now at its lowest level since 1975. It also marks the end of a decade in which total US coal generation was cut in half.”

Several more coal plant closures have already been announced in 2020. This week, Pacificorp announced it will close one coal unit at the Cholla power plant in Arizona this year, the Sierra Club Beyond Coal campaign said that the closure of the Dolet Hills power plant in Louisiana marked the 300th coal-fired power plant announced for retirement since 2010, and Tri-State Generation and Transmission Association announced it will close the Escalante coal plant in New Mexico this year, and the Craig coal plant in Colorado by 2030.