Major banks announce new policies to help push utilities away from coal

Key Points:

- Major financial institutions have announced new policies that limit how they do business with companies that remain reliant on coal.

- Leading financial institutions’ coal exclusion policies assess electric utilities based on how much of their electricity generation mix relies on coal, rather than how much of their revenues rely on coal.

- Some electric utilities in the U.S. have recently highlighted different metrics such as “coal share of rate base,” which can obscure how reliant on coal they remain.

Several major banks have announced new policies in recent months that limit how they will do business with companies that rely on coal, including electric utilities. Those policies vary among financial institutions; some establish clear criteria under which a bank will divest from companies that remain reliant on coal, while others describe how the bank will engage with companies to facilitate a transition away from coal. But nearly all the policies make clear that major banks expect electric utilities to move away from coal over the next decade.

Barclays announced in March 2020 that it aims to become a net zero bank, and published its latest Environmental, Social and Governance report. That report explained how the bank has increased its prohibitions on financing companies that rely on coal, and will further increase those restrictions over the next decade:

We will prohibit financing to clients with more than 50% of their revenue from thermal coal as of 2020, transitioning to 30% as of 2025, and to 10% as of 2030.

BNP Paribas announced in May 2020 that it is “speeding up its timetable for a complete exit from coal” including not “accepting any new customers whose share of coal related revenue surpasses 25%.” The bank also said it aims for electric utilities that it finances to stop using coal by 2030 in the U.S., Europe, and other OECD countries:

BNP Paribas is expanding to all OECD countries its target to end the use of coal by its electricity-producing customers by the end of 2030. The end date for coal use by its electricity-producing customers is now 2030 for the European Union and the OECD, and the commitment to end for the rest of the world in 2040 is maintained.

Citigroup updated its Environmental and Social Policy Framework in April 2020:

For power sector clients with coal-fired power generation, Citi will annually review their greenhouse gas (GHG) reduction strategies and their management of the risks and opportunities related to a low-carbon transition. We will request information on GHG emissions (owned generation and purchased power); climate-related risks and opportunities impacting the client’s business strategy, including, if available, a climate warming scenario analysis; and a description of the company’s current efforts and future strategic plans designed to support its transition to a low-carbon energy future, including diversification options for the company’s mix of owned and purchased generation capacity to shift away from coal-fired power sources; and quantitative targets for reducing GHG emissions.

Morgan Stanley updated its Environmental and Social Policy Statement in April 2020:

We will engage with companies that derive a significant portion of their revenue from coal power generation to understand their strategy to diversify away from coal and reduce their carbon emissions.

Goldman Sachs updated its Environmental Policy Framework in December 2019:

For financings involving any power sector companies that derive a significant portion of their generation from coal, we will engage with the companies to understand their strategy to diversify away from coal, and reduce overall carbon emissions, with the goal of supporting their low carbon transition in line with the Paris Climate Agreement.

BlackRock’s sustainable investment policy announcement in January 2020 attracted global attention, given its role as the world’s largest money manager. BlackRock CEO Larry Fink’s letter to clients outlined BlackRock’s new policies, including divesting from “companies that generate more than 25% of their revenues from thermal coal production.” (e.g., mining companies). The policy also says that BlackRock will “closely scrutinize other businesses that are heavily reliant on thermal coal as an input, in order to understand whether they are effectively transitioning away from this reliance.” (e.g., electric utilities).

At a utility industry conference in February, an American Electric Power executive explained that BlackRock’s coal exclusion policy is “something that needs to be taken to heart” because BlackRock is a major investor in utilities.

Several other financial institutions have also announced policies that restrict how they finance coal plants, mines, and the companies that own and operate them. According to the Institute for Energy Economics and Financial Analysis, over 100 globally significant banks and insurance companies (those with at least $10 billion assets under management) have announced coal exclusion policies. Many of those policies also restrict other fossil fuel projects such as tar sands extraction and Arctic oil drilling, in response to campaigns by Indigenous and environmental groups.

Leading policies assess electric utilities based on coal share of generation, instead of coal share of revenue

The Norwegian Sovereign Wealth Fund has one of the longest-established coal exclusion policies, which it has updated over the years. Its policies make clear that the Norwegian Fund will divest from “coal power companies and mining companies who themselves, or through other operations they control, base 30 percent or more of their activities on coal, and/or derive 30 percent of their revenues from coal.”

That includes several U.S. electric utilities that generate 30% or more of their electricity from coal. Based on its coal exclusion policy, the Norwegian Fund has divested from Allette (Minnesota Power), AES, Alliant, Ameren, American Electric Power, (including subsidiaries Appalachian Power and Indiana Michigan Power), DTE Energy, Duke Energy, Evergy, FirstEnergy, Great River Energy, IDACORP (Idaho Power), MGE Energy (Madison Gas and Electric), NRG Energy, Otter Tail, Pacificorp, PNM (Public Service Company of New Mexico), WEC Energy Group (Wisconsin Electric Power), and Xcel Energy (including subsidiaries Northern States Power, Public Service Company of Colorado, and Southwestern Public Service).

The Norwegian Fund has also placed some companies under “observation,” including several U.S. electric utilities: Berkshire Hathaway Energy, CMS Energy (Consumers Energy), MidAmerican Energy, Northwestern, OGE Energy (Oklahoma Gas & Electric), Pinnacle West (Arizona Public Service), Portland General Electric, Southern Company, and Vistra.

The Norwegian Fund’s policy explains why it includes two different metrics for determining whether a company is heavily reliant on coal: 30% of revenue, or 30% of activities (such as electricity generation). The policy also notes that using percentage of electricity generation is more relevant for electric utilities than percentage of revenue, while percentage of revenue is more relevant for mining companies, because of differences in how companies in those sectors report data:

30 percent or more of revenue from thermal coal

The threshold related to 30 percent or more of revenue is typically more applicable to the thermal coal extraction business than the power industry. The reason for this is that companies in this sector often report revenue values split by extraction related to thermal and met coal which makes measurement against the criteria more transparent.

30 percent or more of their activities on thermal coal

This threshold entails an assessment of what a company bases its business on and is more relevant to companies in the power industry than to mining companies. As an example, companies deriving 30 percent or more of their revenue from self-generated energy production can be identified. The mix of fuel sources used in these companies’ energy production can then be assessed. If 30 percent or more of a company’s aggregate self-generated energy production measured in energy units is based on coal, it will be covered by the criterion.

Similarly, insurance company AXA makes clear that it will divest from “Power generation companies that have 30% or more of electricity generation capacities powered by coal,” in addition to companies that rely on thermal coal for 30% or more of revenue. Swiss Re and Zurich also won’t insure or invest in electric utilities that generate more than 30% of their electricity from coal, while using coal share of revenue for mining companies. Zurich, Swiss Re, and AXA ranked highest in a scorecard of insurance companies’ coal exclusion policies, published in December 2019 by Insure Our Future, a network of environmental and consumer organizations urging insurance companies to stop insuring and investing in coal and tar sands projects. The two top-ranked coal exclusion policies of insurance companies headquartered in the U.S., Axis Capital and Chubb, also specify that the companies will not insure or invest in utilities that generate 30% or more of their power from coal, while using coal share of revenue figures for mining companies.

Reclaim Finance urges financial institutions to use percentage of electricity generation, rather than percentage of revenue, when determining which electric utilities are heavily reliant on coal. The Paris-based organization’s Coal Policy Tool compares and ranks French financial institutions’ coal exclusion policies, and penalizes policies that use percentage of revenue for electric utilities instead of percentage of generation. Reclaim Finance plans to expand its Coal Policy Tool later this year to assess global financial institutions’ coal exclusion policies.

In an analysis of BlackRock’s new policies, a network of organizations pressuring major asset managers called BlackRock’s Big Problem also highlighted the shortcomings of using coal share of revenue to assess electric utilities:

If an exclusion threshold uses a revenue metric, as BlackRock has, instead of a production metric, this can create a problem when this metric is applied to assess utilities. This is especially problematic in places where coal is uneconomical (e.g. certain utilities would slip through the cracks at 25% revenue, due to the uneconomical nature of the business, but would be on the exclusion list using a 25% production metric).

Despite those concerns, some financial institutions are using percentage of revenue to determine which electric utilities are heavily reliant on coal. To help financial institutions make informed decisions about divesting from coal-reliant companies, researchers with the Germany-based organization Urgewald developed the Global Coal Exit List. The list provides key statistics about hundreds of companies around the world, including estimates of the percentage of each company’s revenues that come from coal. Those figures include “all components of the thermal coal value chain,” including transmission and distribution of coal-fired electricity.

A table at the end of this post shows how much major electric utilities in the U.S. rely on coal according to the Global Coal Exit List, as a percentage of electricity generation, as well as a percentage of revenue.

Utilities obscure their reliance on coal with misleading metrics like “coal share of rate base”

As more major financial institutions assess whether the companies with whom they do business are heavily reliant on coal, some electric utilities have sought to emphasize figures other than coal share of generation or coal share of revenue, which can obscure how reliant on coal they remain.

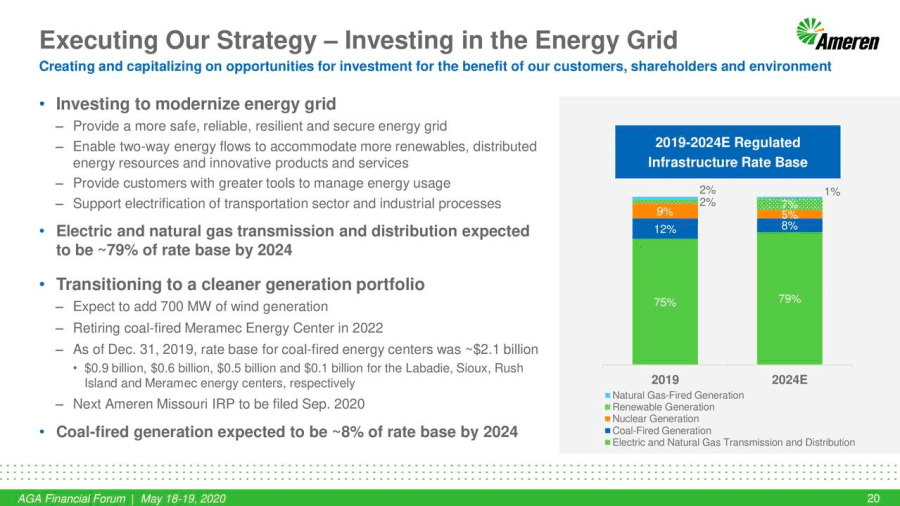

For example, in an earnings call with investors in February 2020, Ameren CEO Warner Baxter told investors that “As a result of Ameren Missouri’s investment in 700 megawatts of wind, combined with the scheduled retirement of the Meramec coal-fired energy center in 2022, we expect coal-fired generation to decline to just 8% of rate base by year-end 2024.” (“Rate base” is the value of a utility’s assets, less appreciation; it is the part of a utility’s spending on which it is allowed to earn a profit by regulators.)

Ameren also noted that “Coal-fired generation expected to be ~8% of rate base by 2024” in a presentation last week to the American Gas Association Virtual Financial Forum.

But Ameren’s plans to close the Meramec coal plant actually amount to only a modest shift away from coal. The utility will continue to operate three other larger coal plants for more than a decade (Labadie, Rush Island, and Sioux); the 873 megawatt Meramec coal plant represents only 17% of Ameren’s total 5,395 megawatt coal capacity. Without plans to close the rest of its coal fleet, Ameren’s generation mix would remain dominated by coal in 2030, as a March 2019 report by the utility makes clear.

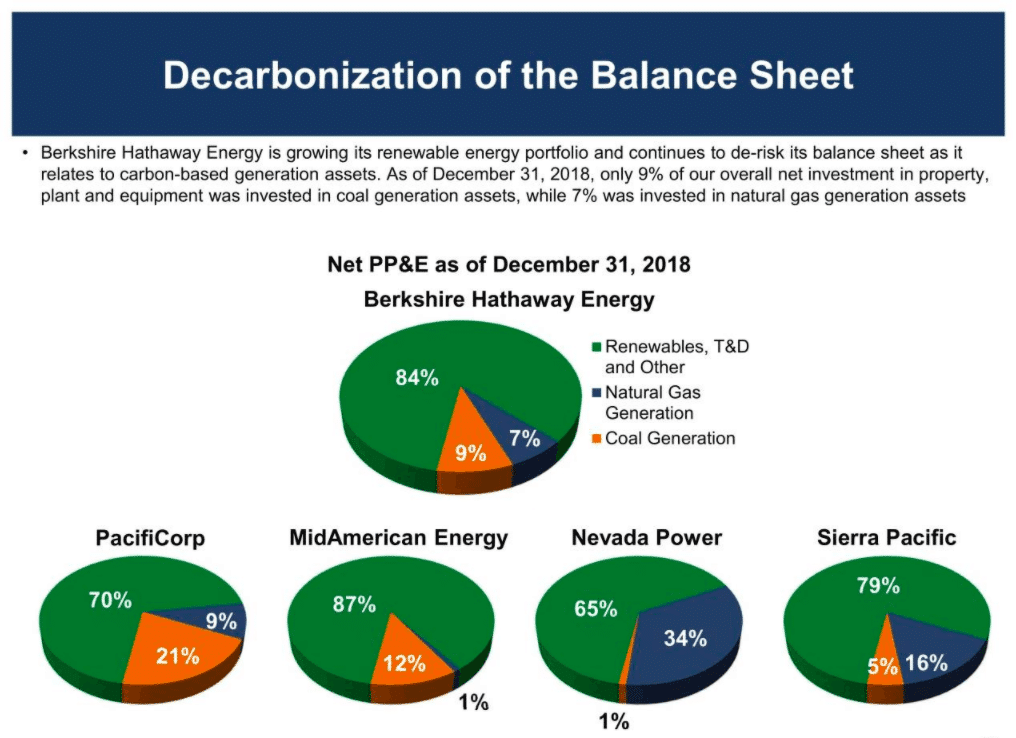

In a presentation at the Edison Electric Institute Financial Conference in November 2019, an executive with Warren Buffett’s Berkshire Hathaway Energy said that “only 9% of our overall net investment in property, plant and equipment was invested in coal generation assets, while 7% was invested in natural gas generation assets.”

The slide also reported the percentages that coal and gas generation accounted for of total investment in property, plant, and equipment for Berkshire Hathaway Energy’s subsidiaries Pacificorp, MidAmerican Energy, NV Energy, and Sierra Pacific. While the slide states that coal accounts for 21% of Pacificorp’s net investment in property, plant, and equipment, Pacificorp’s generation mix remains dominated by coal, at 56%. Pacificorp has announced plans to close some of its coal plants over the next decade and add more wind and solar, but that plan will also leave other coal plants running.

Coal’s share of a utility’s rate base can be relevant information for investors, since it can help investors determine which utilities are better positioned to increase profits by replacing coal with renewable energy. But “coal share of rate base” metrics ignore the risks facing utilities that continue to rely on coal for significant portions of the electricity they generate, and can present a misleading picture of how far many electric utilities are from a transition away from coal.

Coal share of revenue estimates for U.S. power companies

The table below shows U.S. power companies’ coal share of generation and coal share of revenue, using figures from the Global Coal Exit List. Coal Share of Power Production figures are percentage of generation, except those in italics which are percentage of capacity. Subsidiaries are listed under their parent companies. Figures are generally for 2018, but are sometimes for earlier years when 2018 data was not available. Figures for other companies, and more details about methodology, are available at https://coalexit.org/

|

Company (Parent Company) |

Coal

Share of Power Production |

Coal

Share of Revenue |

|

AES Corporation |

33% |

>30% |

|

Dayton Power and Light

Co (AES Corporation) |

100% |

NA |

|

Indianapolis Power &

Light Co (AES Corporation) |

44% |

>30% |

|

Allete Inc. |

70% |

>30% |

|

Minnesota Power (Allete Inc.) |

>30% |

>30% |

|

Alliant Energy Corp. |

40% |

34% |

|

Interstate Power &

Light Co (Alliant Energy Corp.) |

35% |

NA |

|

Wisconsin Power &

Light Co (Alliant Energy Corp.) |

41% |

NA |

|

Ameren Corporation |

71% |

61% |

|

Ameren Missouri (Ameren

Corporation) |

71% |

68% |

|

American Electric Power Co Inc |

60% |

>30% |

|

Appalachian Power Co

(AEP) |

77% |

>50% |

|

Indiana Michigan Power

Co (AEP) |

36% |

>30% |

|

Kentucky Power Co (AEP) |

88% |

>50% |

|

Southwestern Electric

Power Co (AEP) |

80% |

>50% |

|

Wheeling Power Co (AEP) |

100% |

100% |

|

Public Service Company

of Oklahoma (AEP) |

44% |

>30% |

|

AEP Generating Company

(AEP) |

100% |

>90% |

|

Associated Electric Cooperative Inc |

63% |

>50% |

|

Basin Electric Power Cooperative |

65% |

62% |

|

Berkshire Hathaway Energy Company |

50% |

<30% |

|

PacifiCorp (Berkshire

Hathaway Energy Company) |

68% |

>50% |

|

MidAmerican Energy Co

(Berkshire Hathaway Energy Company) |

47% |

>30% |

|

MidAmerican Funding LLC

(Berkshire Hathaway Energy Company) |

47% |

NA |

|

NV Energy (Berkshire

Hathaway Energy Company) |

10% |

<20% |

|

Big Rivers Electric Corp |

100% |

>90% |

|

Black Hills Corp |

63% |

37% |

|

CenterPoint Energy Inc |

80% |

NA |

|

CMS Energy Corporation |

47% |

19% |

|

Consumers Energy Company

(CMS Energy Corporation) |

61% |

20% |

|

DTE Energy Co. |

65% |

>30% |

|

Duke Energy Corporation |

31% |

28% |

|

Duke Energy Carolinas

LLC (Duke Energy Corporation) |

33% |

>30% |

|

Duke Energy Indiana Inc

(Duke Energy Corporation) |

71% |

>50% |

|

Duke Energy Progress LLC

(Duke Energy Corporation) |

28% |

<30% |

|

Duke Energy Florida LLC

(Duke Energy Corporation) |

14% |

<30% |

|

Duke Energy Ohio Inc

(Duke Energy Corporation) |

56% |

>30% |

|

Empire District Electric Co |

41% |

NA |

|

Evergy Inc |

43% |

>30% |

|

Kansas City Power &

Light Co (Evergy Inc) |

43% |

>30% |

|

KCP&L Greater

Missouri Operations (Evergy Inc) |

21% |

<30% |

|

FirstEnergy Corp |

86% |

>30% |

|

Tucson Electric Power Co (Fortis Inc) |

51% |

>50% |

|

GenPower

Holdings LP / Longview Power LLC |

100% |

100% |

|

Great River Energy |

58% |

>30% |

|

Hoosier Energy |

57% |

>50% |

|

Intermountain Power Agency |

100% |

100% |

|

Lower Colorado River Authority |

36% |

<30% |

|

MGE Energy Inc |

68% |

>30% |

|

Montana-Dakota Utilities Co |

46% |

NA |

|

NiSource |

77% |

28% |

|

Northern Indiana Public

Service Company, Inc. (NiSource) |

73% |

>50% |

|

Northwestern Corp |

39% |

<30% |

|

NRG Energy Inc |

48% |

<30% |

|

OGE Energy Corp |

54% |

>30% |

|

Ohio Valley Electric Corporation |

100% |

100% |

|

Omaha Public Power District |

71% |

>50% |

|

Otter Tail Corporation |

84% |

41% |

|

Otter Tail Power Co

(Otter Tail Corporation) |

84% |

>50% |

|

PNM Resources Inc |

45% |

34% |

|

Public Service Company

of New Mexico (PNM Resources Inc) |

45% |

>30% |

|

PPL Corporation |

85% |

>30% |

|

Kentucky Utilities Co

(PPL Corporation) |

82% |

>50% |

|

Louisville Gas &

Electric Co (PPL Corporation) |

90% |

>50% |

|

Prairie State Generating LLC |

100% |

>90% |

|

Prairie State Energy

Campus LLC (Prairie State Generating LLC) |

100% |

>90% |

|

Santee Cooper |

53% |

>30% |

|

Southern Company |

30% |

<30% |

|

Georgia Power Co

(Southern Company) |

30% |

<30% |

|

Alabama Power Co

(Southern Company) |

50% |

>30% |

|

Mississippi Power Co

(Southern Company) |

7% |

<20% |

|

Sunflower Electric Power Corporation |

53% |

>30% |

|

Talen Energy |

42% |

>30% |

|

TransAlta Holdings U.S. Inc (TransAlta Corporation) |

86% |

>50% |

|

Tri-State Generation & Transmission Association |

41% |

>30% |

|

Vistra

Energy Corp |

34% |

>30% |

|

Luminant (Vistra Energy Corp) |

28% |

NA |

|

WEC Energy Group Inc |

40% |

<30% |

|

We Energies (WEC Energy

Group Inc) |

39% |

NA |

|

Wisconsin Public Service

(WEC Energy Group Inc) |

40% |

>30% |

|

XCEL Energy Inc |

33% |

<30% |

|

Northern States Power Co

(XCEL Energy Inc) |

30% |

26% |

|

Public Service Company

of Colorado (XCEL Energy Inc) |

40% |

30% |

|

Southwestern Public

Service Company (XCEL Energy Inc) |

30% |

30% |